Venture capital (VC) has played a pivotal role in funding innovation and high-growth startups over the past decades. However, the industry is now facing winds of change.

Venture Capital Firms (VCs) play a critical role by aggregating funds from their pool of investors and funneling these resources towards entrepreneurs with promising and innovative proposals. This symbiotic relationship allows investors to potentially achieve returns that surpass those of equivalent public markets, while simultaneously enabling startups to secure the necessary capital to cultivate and bring their novel business ideas to fruition.

INDUSTRY SNAPSHOT

In the first quarter of 2023, global VC funding reached $76 billion, marking a 53% decline compared to the first quarter of 2022

This decline in funding was despite the inclusion of two large deals: a $10 billion investment into OpenAI and a $6.5 billion round for Stripe

Without these two large deals, Q1 venture funding would have been even lower, close to $60 billion

Despite the decline in overall funding, there was a surge in global venture investments in the first quarter of 2023, thanks to the record fundraising rounds by OpenAI and Stripe

In 2022, the top three countries globally for venture capital investment were the United States, China, and the United Kingdom

In 2021, global VC investment rose to a record $671 billion across 38,644 deals, with a dramatic increase in valuations and deal sizes

Corporate venture capital (CVC) remained strong, reaching $81 billion in Q4 2021

In Q4 2022, VC investment globally dropped for the fourth straight quarter, but it remained comparable to the levels seen prior to the onset of the Covid-19 pandemic

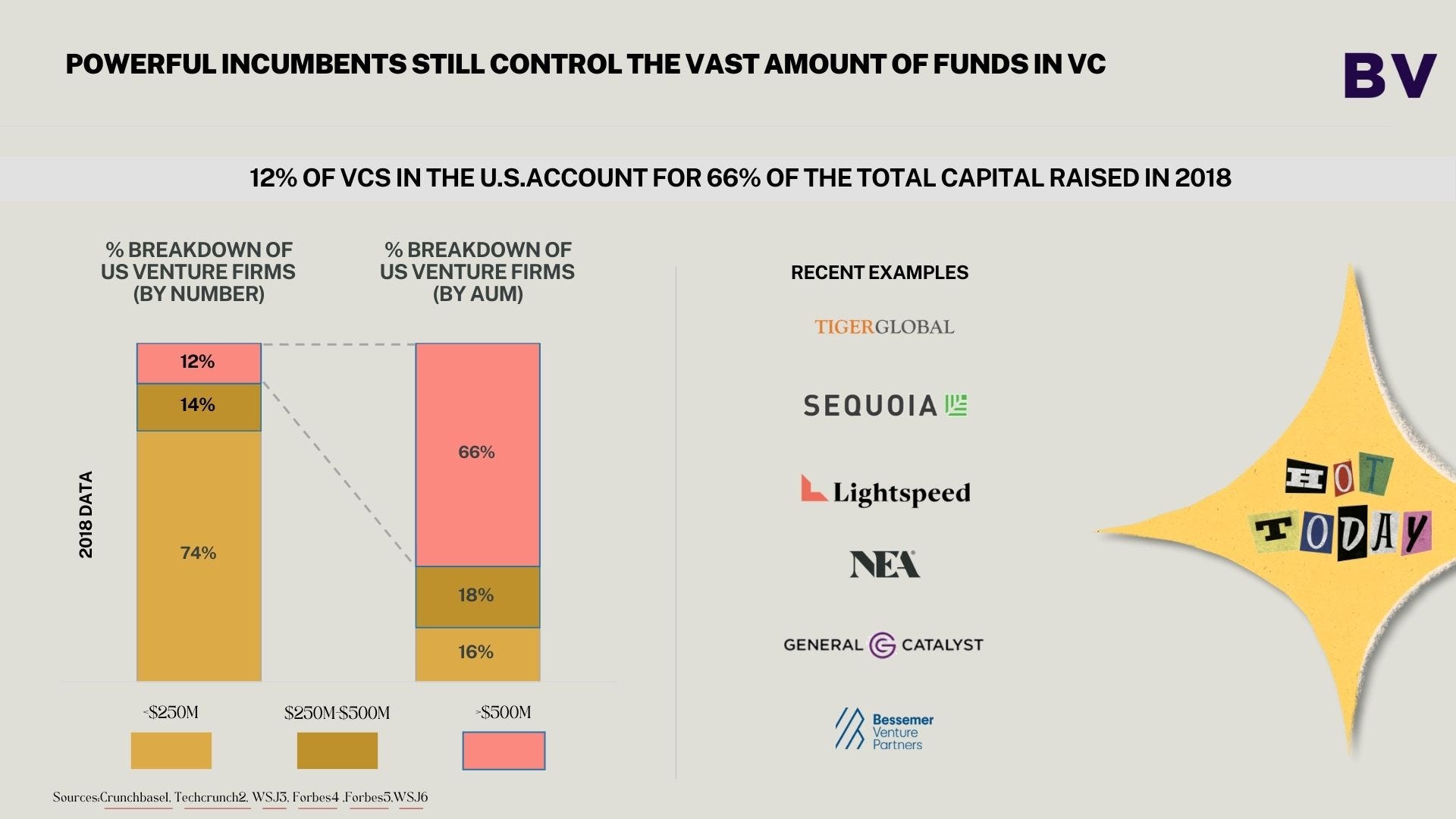

Powerful incumbents control a vast amount of funds in VC

12% OF VCS IN THE U.S. ACCOUNT FOR 66% OF THE TOTAL CAPITAL

Notable Examples:

Tiger Global: Raised $7.5 billion recently from two separate funds; one was raised in January 2021 and the other was closed a year before.

Sequoia: Raised $7.2 billion for new funds to deploy in China, India and the U.S in July 2020.

Lightspeed: Raised $4.2 billion across 3 funds globally in April 20204.

NEA raised $3.6 billion in March 2020, bringing its total capital under management to nearly $24 billion.

General Catalyst: Raised $2.3 billion in capital commitments across three funds in March 2020.

Bessemer Venture Partners: Raised $1.85 billion in 2018 for its 10th fund, its largest fund to date.

How are Traditional VCs Maintaining a Strong position?

Prestigious Brands: A distinguished legacy and reputation established by notable General partners

Proven Performance and Judgement: Unvarying high-yield returns enable these VCs to attract more investors.

Attention from Entrepreneurs: Startups receive significant value recognition by aligning themselves with the top VCs.

Guidance and Expertise: Capability to offer strategic and operational insight to aid founders in expanding their businesses

Abundant Deal Flow Opportunities: Exposure to a vast number of start-ups consistent with the relevant investment philosophy.

Significant Resources: Potential to offer non-financial resources such as introductions to leading startups in the portfolio and connections with large corporations.

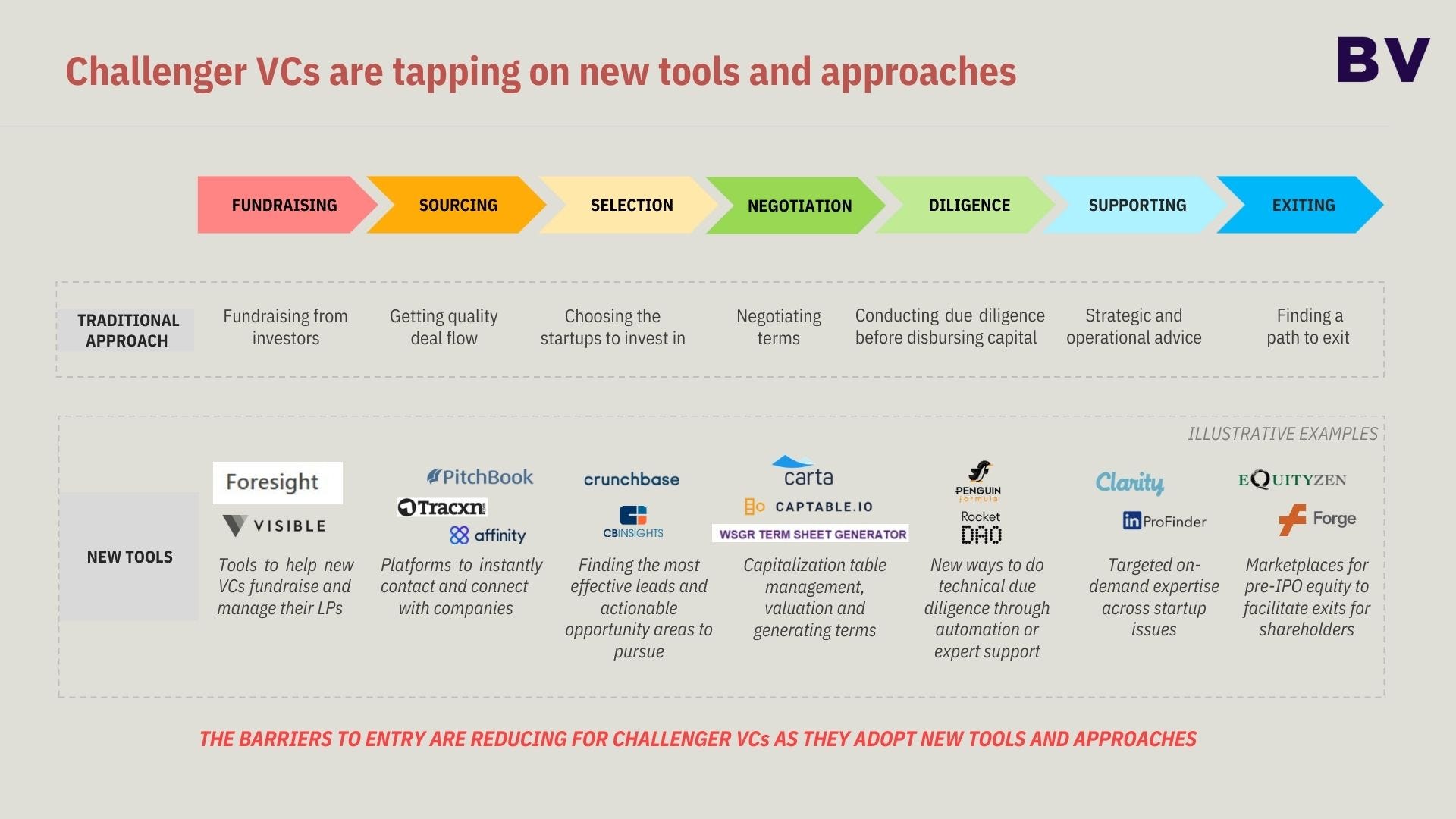

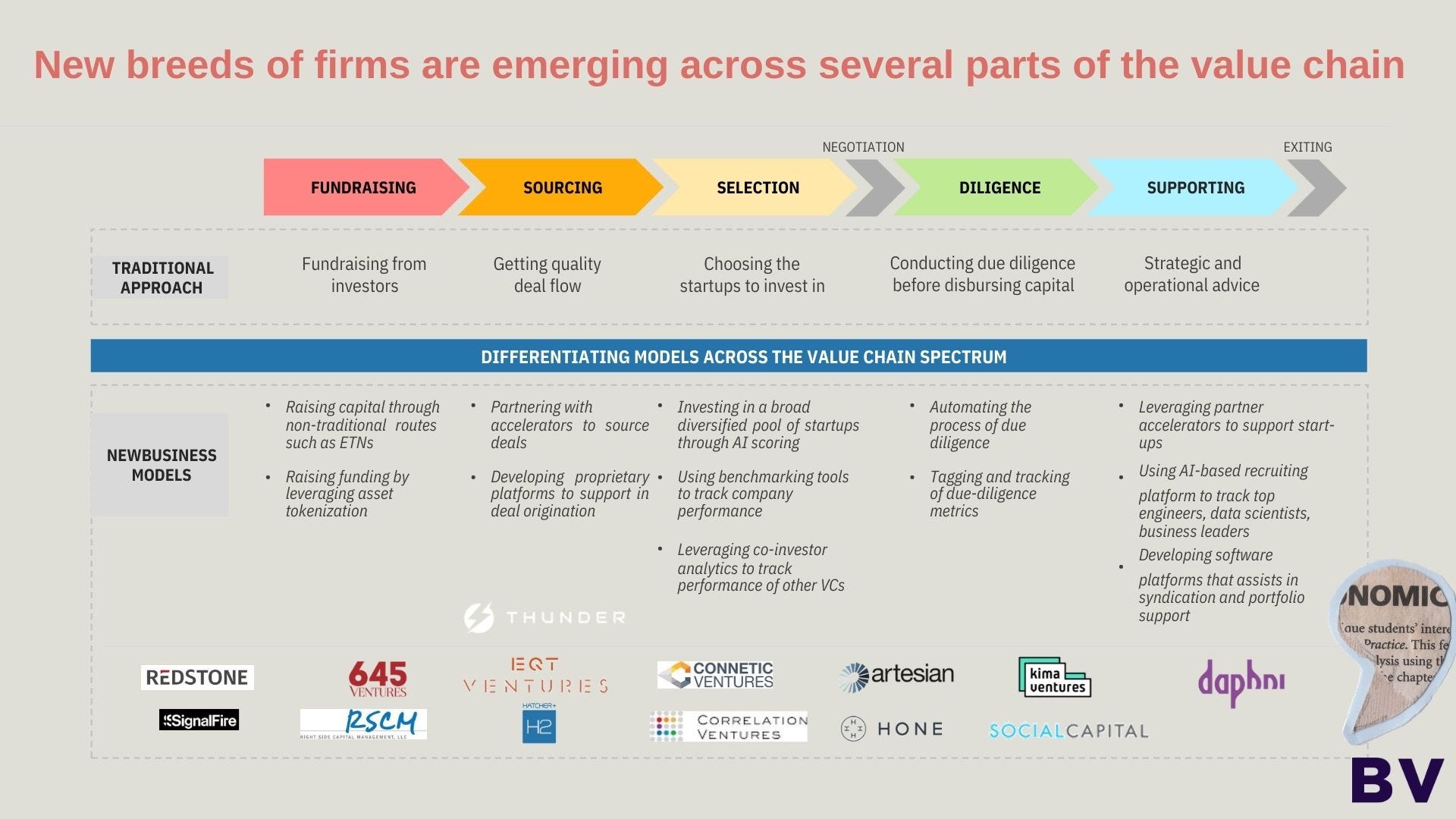

The VC value chain is profoundly interconnected and depends on human connections, identifying patterns, and sound judgment.

The venture capital industry is encountering four major transformations

Democratization

The democratization of venture capital investment is a profound development, echoing a broader societal movement towards inclusion and accessibility.

Key Insights:

Increased Access: Corporates, family offices, and other non-traditional investors entering the VC space leads to a more diversified ecosystem, reflecting the societal shift towards inclusion.

Ubiquitous Technology: This plays an essential role in lowering barriers for startups, enabling more innovators to bring their visions to life without exorbitant entry costs.

Alternative Financing Routes: The surge in bootstrapping and alternate financing adds vibrancy and resilience to the entrepreneurial ecosystem.

Deal-Growth

A significant transformation is seen in the dynamics of deal-making, fueled by readily available capital and an evolving investment paradigm.

Key Insights:

Increased Capital Availability: Low interest rates and abundant dry powder in PE/VC indicate a more aggressive investment environment.

Rise of Mega Rounds: These replace traditional IPOs, indicating a more private market's dominance.

Micro and Nano VCs: The rise of these entities is a sign of diversification within the investment space, enabling more nuanced investment strategies.

Diversification

The expansion of VC activity into various markets and sectors adds resilience and offers new opportunities.

Key Insights:

Emerging Markets: The growth in China, India, Latin America, Africa, and Southeast Asia marks a globalized venture capital trend.

ESG Investing: This reflects a paradigm shift in investor thinking, aligning profitability with sustainability.

Gender and Diversity Gaps: Increased awareness can lead to more equitable funding and inclusive growth.

Digitization

A defining trend of our era, the integration of digital technologies into VC, creates efficiency and adds analytical rigor.

Key Insights:

Data Utilization: The exponential growth in data and analytics empowers better decision-making.

Automation: Replacing manual tasks with automation creates efficiency, allowing a focus on strategic elements.

AI in Decision-Making: Integrating AI can enhance precision and offer insights beyond human analysis.

Whether it's the democratization of access, the growth in deal activity, diversified investment strategies, or the integration of cutting-edge technologies, these trends provide a roadmap for a more inclusive and adaptive future in venture capital.

Initial indications of potential disruptions within the VC industry are surfacing

Disruptive patterns are beginning to emerge in the venture capital industry, and non-players fueled by capital are rapidly entering with new business models and technology.

There appears to be a notable decrease in investor loyalty, which might be attributed to overshooting, although there's no substantial evidence or observations of incumbents oversatisfying investor needs. However, it can be noticed that investors are displaying lower loyalty to individual funds and are increasingly getting involved in funds of funds, which suggests a significant and lasting change in their investment behavior.

There's been a remarkable and enduring surge in capital inflows, along with a rise in the number of new venture capital firms and funds. This includes the emergence of large-scale funds, or "mega-funds." Additionally, a broader range of entities are actively engaging themselves within the Venture Capital industry, indicating an expanding ecosystem.

Changes in policy are fostering an environment conducive to new entrants. Regulations are being eased, rules are becoming simpler, and barriers to investors are decreasing, all contributing to an influx of new funds and participants into the marketplace.

New entrants are popping up at the lower end of the market or on the periphery with solutions that may initially appear inferior. Also, there's an emergence of innovative investment strategies being implemented by smaller and newer venture capital firms. These strategies include approaches like smart-beta, predictive artificial intelligence, venture debt financing, crowdfunding, and initial coin offerings (ICOs).

Investor habits and preferences are starting to display a shift. Specifically, newer investors, such as high-net-worth individuals (HNWIs) and corporate venture capitals (CVCs), are entering the venture capital space with different objectives in mind. New offerings like Venture-as-a-Service (VaaS) are facilitating their active involvement in the sector.

A viable competitor fine-tunes a disruptive business model.Existing players in the market are investigating and adopting new models and strategies to remain competitive. This includes tactics like leveraging start-up founders to source deals and partnering with consulting firms, among others.

As revenue growth from fund fees decreases, profit margins are simultaneously expanding. Despite these dynamics, capital continues to pour into VC funds, thus generating increasing revenues from fees. However, it's worth noting that investors may seek more cost-effective methods to participate in venture capital. For example, platforms like the AngelList Access Fund offer an appealing 1% in fees, appealing to cost-conscious investors.

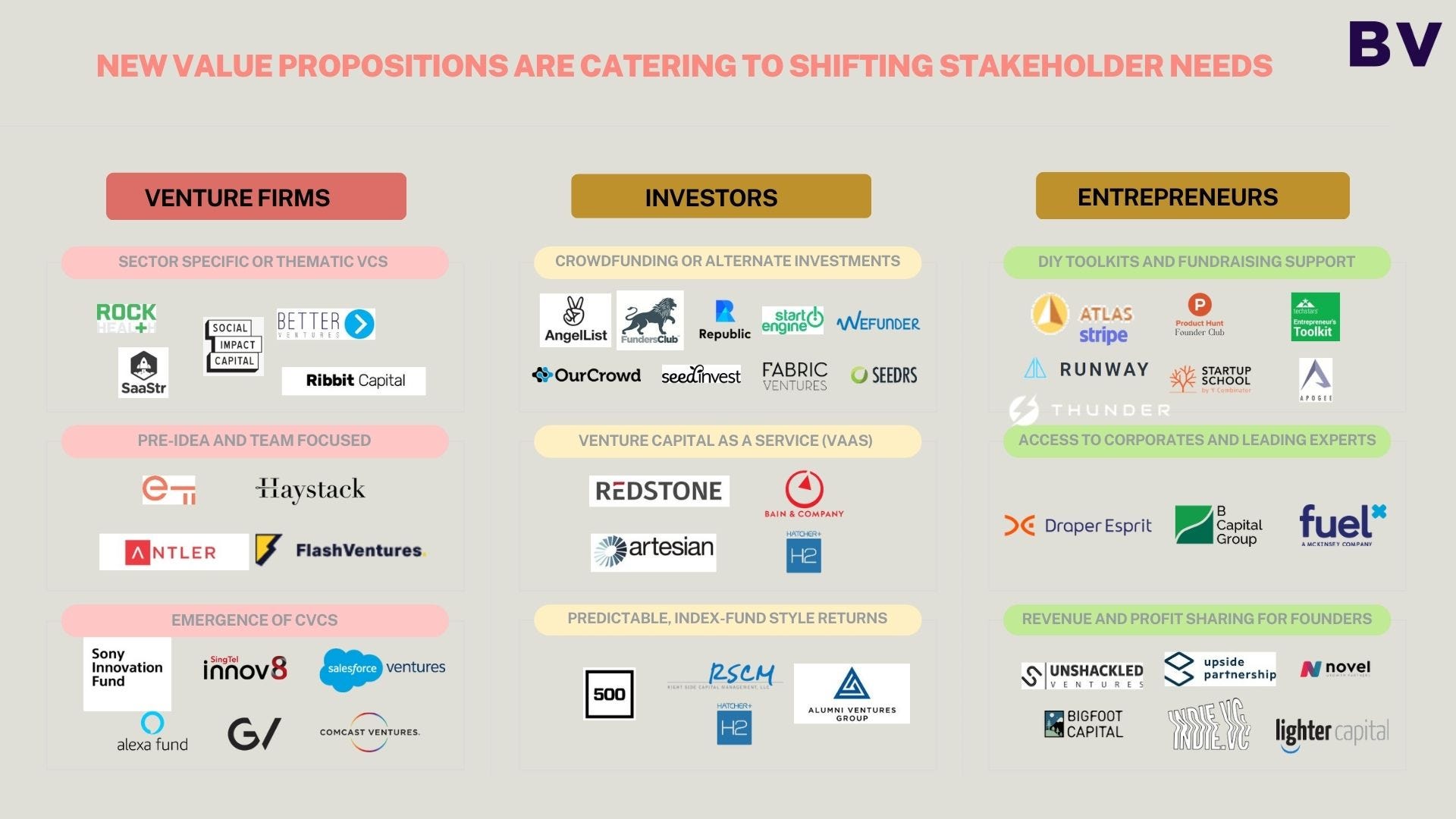

New tools and Approaches

New Breeds emerging across the Value Chain

New Value Propositions Catering an Evolving Landscape

This perfect storm is creating openings for new entrants and alternative models: direct online investing, AI-powered seed investing, indexing approaches, and models offering VC-as-a-service. Many leverage revenue-based financing and tailored offerings for angels, family offices, and corporations.

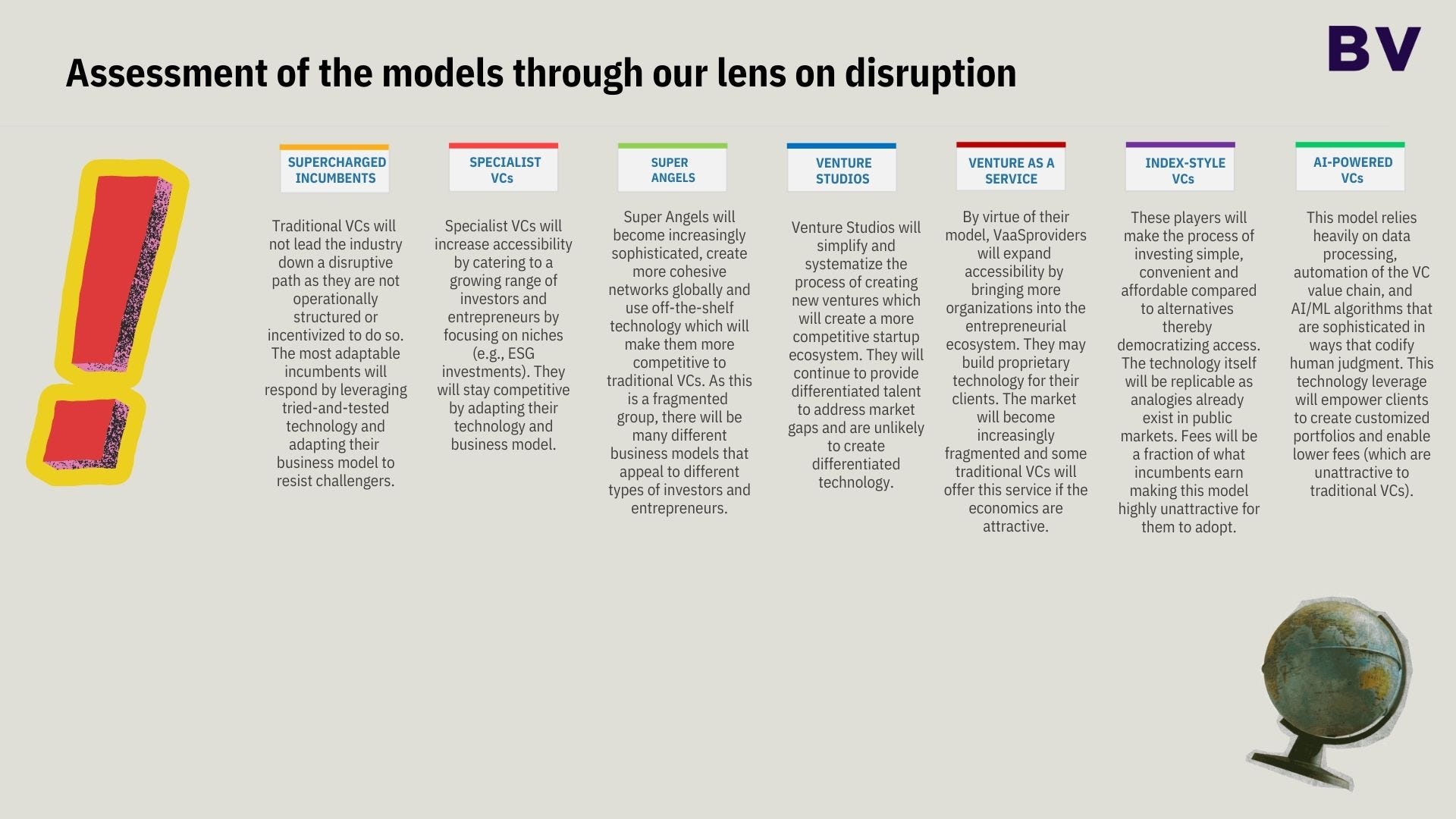

Supercharged incumbents are Traditional VCs who adopt new business models and technology in venture investing

Specialist VCs, those offering niche specialization (B2B SaaS, social impact) and value-add services

Super Angels, angel investors who have become more sophisticated and professionalized their operations

Venture Studios are VCs that invest resources in creating start-ups from the ground up based on an outlier team or pre-identified opportunity areas

Venture as a Service, for organizations and individuals to empower them to launch their own fund

Index-Style VCs, which have a large, global, diversified portfolio of private investments into startups

AI-powered VCs, those whose investment decisions and other value-add services are driven by AI

Disruptive VCs must answer 3 questions

Does the solution make it more simple, convenient, accessible, or affordable for people to address a problem that matters to them?

Does the solution feature a difficult-to-replicate technological core?

Does the solution involve a business model that looks structurally unattractive to incumbents?

Challenger VCs

To ensure long-term success, challenger Venture Capitalists must validate their business models. First, they must establish a history of robust and reliable returns. Second, they need to develop unique data and exclusive technology that's difficult to copy. Third, their economics—including fees, carry, and financing models—should be tailored to attract varying investors and startups. Fourth, and most importantly, they should confirm that their models are sustainable and capable of scaling up.

Incumbents

To thrive in the long run, incumbent businesses must adapt and evolve their methods. This begins by transforming the unconventional aspects of human judgment and intuition into a systematic and repeatable process. Alongside this, they should also embrace emerging technologies like Artificial Intelligence (AI) and Machine Learning (ML) to source and analyze deals, enhancing their competitiveness in this rapidly changing landscape. Paying attention to non-traditional investors is also a crucial aspect, as these groups are becoming increasingly significant within the venture ecosystem and can offer fresh and unique perspectives. Lastly, incumbents should use their resources, connections, and extensive portfolios of global startups as a catalyst for cross-learning. This way, they can create synergies that benefit both themselves and their portfolio companies, fostering an environment of growth and development.