Worldwide Macroeconomic Forecast

July 2023

Executive summary

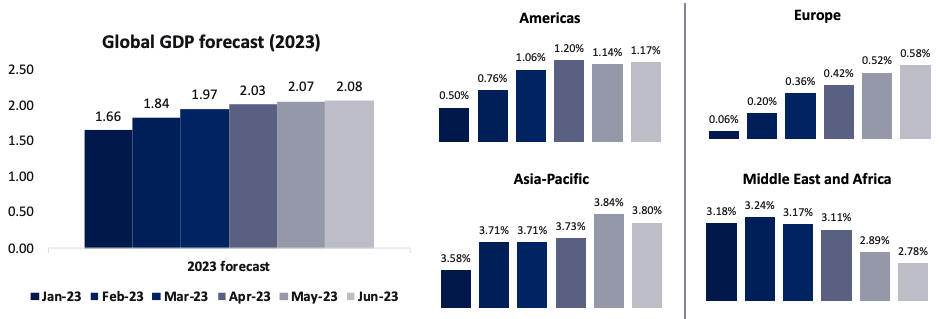

Global growth projection for 2023

June 2023 resulted in a 0.11 percentage point increase in the global real GDP growth forecast, compared to the March 2023 update. This positive revision can be attributed to the decrease in energy and food prices and the expected robust performance of Asia-Pacific nations, particularly India and China. Furthermore, all regions, except for the Middle East and Africa, saw an upward revision in their economic growth projections for 2023, in the June 2023 update.

Overall inflationary pressure eases but core inflation still exhibits rising trend in major economies

The global inflation rate is estimated to decrease to 5.3% in 2023 from 8.7% in 2022, but it is projected to remain above the target set by major economies' central banks. Inflation rates are expected to ease across all regions, including the Americas (9.9% in 2023, compared to 10.4% in 2022), Asia-Pacific (6.6% vs 7.6%), Europe (7% vs 11%), and the Middle East & Africa (16% vs 19%), as per GlobalData estimates.

China’s economy to slowdown in H2 2023

China's economy experienced an average annual growth of 5.5% in H1 2023 but is expected to slowdown to 4.7% in Q3 and 5.2% in Q4 2023, due to sluggish demand impacting key economic indicators, according to GlobalData projections.

Cost of financing to stay high

In June 2023, the Federal Reserve paused its rate hike cycle after increasing its rates 10 times since February 2022. However, the European Central Bank continued its streak of rate hikes with the eighth consecutive increase in June 2023. Other major economies also raised rates in the first half of 2023. Despite some easing of inflationary pressure, it remains significantly above the central bank's target. GlobalData predicts that central banks will maintain higher policy rates until inflation falls within their target range.

Business and consumer confidence exhibit varying trends

Business confidence remained low due to high financing costs and lower external demand, while consumer confidence improved due to the easing of inflationary pressures in the first six months of 2023.

Labor market recovery to remain shaky

Unemployment rates are set to increase in the Americas, Arab States, and Europe, while the Asia-Pacific region is expected to see a decline in 2023. Youth unemployment remains a pressing issue, with the highest rates anticipated in developing nations.

Trade prospects remain bleak

Global trade prospects in 2023 are expected to be impacted by lower external demand and higher financing. The World Trade Organization (WTO) projects a growth of 1.7% in global trade volume for 2023, a slowdown from the 2.7% growth recorded in 2022.

Stock market

US stocks excelled in H1 2023, while European and Asian markets rebounded. India's stock market boomed, becoming the world's fourth most valuable.

Global Economy

2023 Economic Growth Forecast: Global/Region

Over the past six months, economic growth projections have been revised upward for most regions, except for the Middle East and Africa. This positive revision can be attributed to the easing of inflationary pressure. Meanwhile, the MEA region's growth prospects in 2023 will be affected by OPEC+ nations cutting oil production, declining oil prices, and reduced external demand.

Economic growth forecast & probability of recession in 2023

Most European Union nations are expected to bypass recession in 2023. Among G20 economies, major countries in Asia-Pacific region, such as India and China, are anticipated to exhibit highest growth rates, positioning them as the fastest-growing economies in 2023.

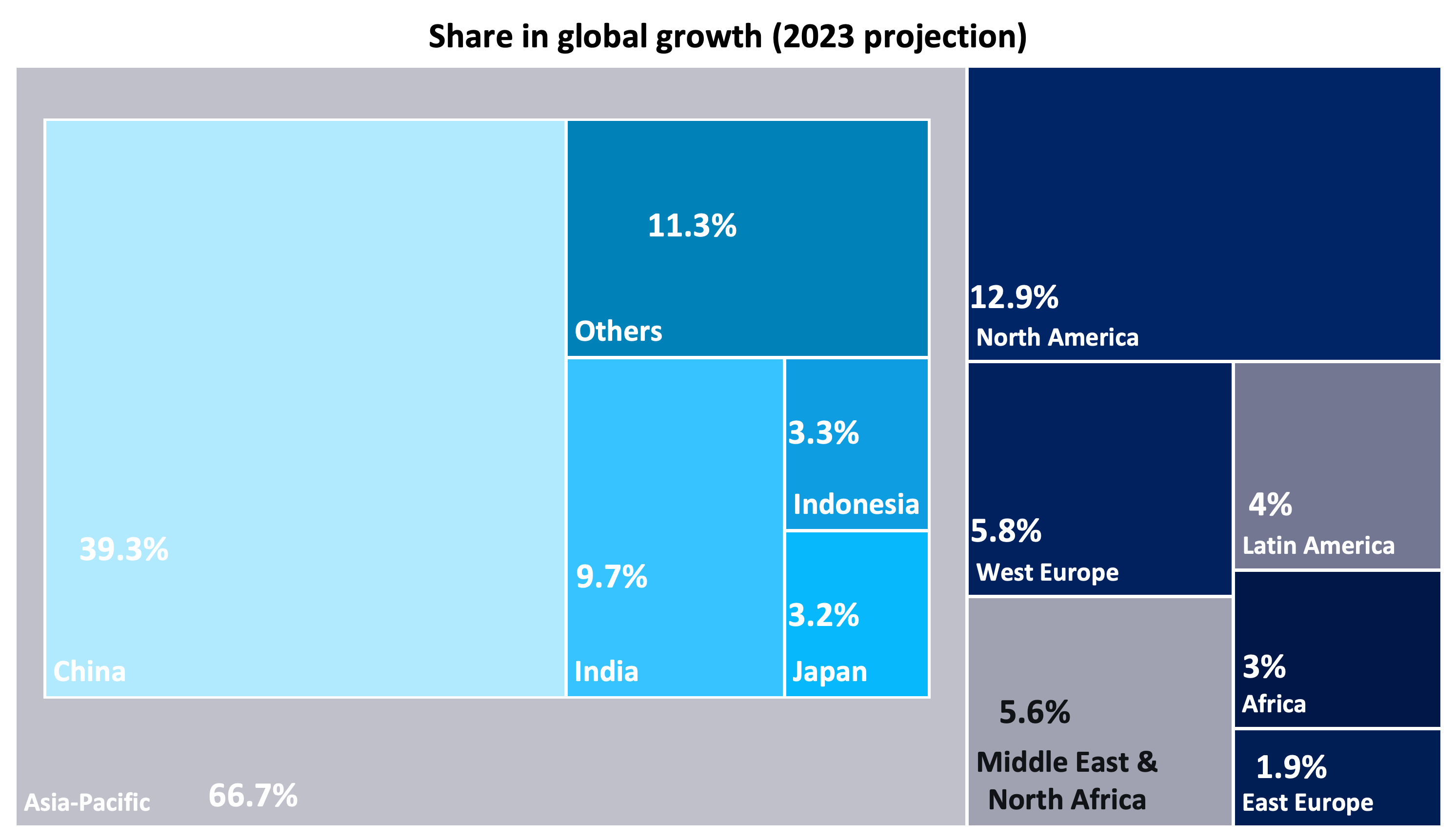

Asia-Pacific region to drive global growth in 2023

In the upcoming year of 2023, the Asia-Pacific region is projected to seize a staggering 66.7% share of global growth, eclipsing the combined contributions of Europe and the Americas at a modest 24.6%. Additional growth impetus is anticipated to stem from the Middle East and Africa, accounting for 8.7%, as per estimations by GlobalData.

Projections indicate that India and China, the economic behemoths of the region, will collectively contribute an impressive 49% to the global growth in 2023, solidifying their pivotal roles on the global stage.

Despite the sluggishness witnessed in the economies of the United States and the European Union, the Asia-Pacific (APAC) region is poised to unveil robust economic growth in 2023. This progress will be significantly propelled by the resurgency in mainland China's economy, facilitated by the easing of COVID-19 restrictions.

India, while experiencing some indications of a potential slowdown, continues to demonstrate remarkable economic expansion and remains one of the fastest-growing economies worldwide. This vibrant growth narrative is reinforced by the flourishing trends of private consumption.

Within the APAC region, the revival of international tourism is proving to be a boon for countries such as Thailand, Malaysia, and Singapore, firmly boosting their service sector exports. Simultaneously, nations reliant on commodity exports, including Australia, Malaysia, and Indonesia, are reaping the benefits of soaring global commodity prices, further elevating their economic fortunes.

In conclusion, the Asia-Pacific region is emerging as an undeniable force in global growth dynamics, capturing the lion's share of progress in 2023. It illustrates a distinctive resilience and a dynamic economic trajectory amid the sluggishness experienced by traditional economic powerhouses. With a rich tapestry of factors fueling its expansion, the Asia-Pacific region stands poised to chart a unique and prosperous path to success.

Europe showing a gradual recovery

•The European nations are anticipated to experience a gradual recovery in growth following a significant downturn. Despite initial projections after the invasion, the economy surpassed expectations in 2022, due to its swift policy responses and a strong rebound in contact-intensive services.

•However, economic activity weakened notably in the latter part of the year, resulting in a mild technical recession in early 2023. Factors such as tightening financial conditions, declining real wages, and diminished consumer confidence due to surging price levels contributed to this decline.

•Although growth is expected to pick up slightly throughout 2023 and 2024, supported by a slow recovery in real incomes, alleviation of supply constraints, and increased external demand, financial conditions will remain challenging. Looking ahead, the output is likely to remain below pre-war trends for an extended period due to adjustments required to adapt to persistently higher energy prices.

•Although inflation has reached its peak, achieving the 2% target remains distant. While headline inflation has decreased significantly since late 2022 due to lower energy prices, core inflation has shown more resilience and has only recently started to decline. This can be attributed partly to the delayed impact of reduced commodity prices on consumer prices and companies' ability to maintain or increase profits. Looking ahead, inflation is expected to continue its downward trajectory, influenced by tight financial conditions curbing demand.

•Contrary to initial concerns, the energy crisis is expected to have positive implications for the transition to green energy. The solidarity among European countries, efforts to diversify energy sources, and the ability of the private sector to adapt have significantly reduced short-term energy security risks. The higher energy prices have incentivized energy efficiency measures, increased cost attractiveness of renewable electricity production, and accelerated the implementation of green policies.

Inflation is showing a downward trajectory

In advanced economies, the falloff in overarching inflation rates can be traced back to lower energy expenses and a steadier supply chain. Yet, upon examining central inflation, which skirts around the fluctuations of food and energy costs, attaining the central banks' goal of 2.0% inflation appears improbable. This scenario unfolds largely due to sustained robust wage advances, leading companies to offset these rising costs through price elevation for consumers.

Energy price eases

Supported by the continuation of OPEC+ oil production curtailment extending to 2024, a forecasted sequential decline in world oil stocks is anticipated over the successive five quarters. This shrinkage is projected to exert an ascent in the pricing benchmark of crude oil, anticipated to be particularly noticeable towards the end stages of 2023 and the initial phase of 2024. The Energy Information Administration (EIA) predicts the average spot price of Brent crude oil to surge to $79 per barrel in the latter half of 2023, touching $84 per barrel in 2024. Regarding international oil utilization, a surge in daily consumption is likely in 2023 - up by 1.6 million barrels from an average of 99.4 million barrels the preceding year. Furthermore, consumption is likely to climb another 1.7 million barrels daily in 2024, largely driven by non-OECD countries.

By June 2023, the EIA anticipates U.S. dry natural gas output to stabilize around an average of 103 billion cubic feet daily (Bcf/d) in the latter half of 2023, a marginal drop from 104 Bcf/d estimated in April and May 2023. This downward shift in production results from diminished drilling operations specifically oriented towards natural gas, influenced predominantly by the significant plunge (over 75%) in the Henry Hub natural gas spot price since its zenith in August 2022.

In H1 2023, the sentiment among businesses and consumers displays divergent trends

There has been a rise in the consumer confidence index over the past three months (March 2023-May 2023), with an increase of 1.2% in the EU27, 0.9% growth in the G20, and a modest leap of 0.5% in the G7 nations, relative to the preceding trilogy of months (December 2022-February 2023).

Contrasting this, the business confidence index over the identical chronological span (March 2023-May 2023) saw a tapering off by 0.6% in EU27, 0.2% in G20 nations, and a slight dip of 0.1% in the US, juxtaposed to the prior trimester (December 2022-February 2023). Interestingly, the index observed a plateau for G7 nations within the corresponding timeline.

The Global Supply Chain Pressure Index plunges to an all-time low, indicating alleviation from logistic constrictions.

In May 2023, the Global Supply Chain Pressure Index, unveiled by the Federal Reserve Bank of New York, plunged to an unprecedented nadir, signifying a considerable abatement in the chokepoints that have been fuelling inflation in preceding years. This index, which quantifies the afflictions endured by universal supply chains, fell from -1.35 to -1.71, relative to the prior month, reaching its lowest point since inception of data gathering in 1997. It is noteworthy that it hit its apex at 4.31 in December 2021.

The New York Fed emphasized that the index's fall had main roots in the shrinking of backlogs in the UK and delivery times in Taiwan. On the flipside, delivery times and backlogs in the Eurozone ushered in upward thrust on the index in May 2023. A probe into the supporting details divulges that all regions surveilled by the Global Supply Chain Pressure Index currently swim below their past averages.

This pronounced drop in the index, housing 27 components, such as worldwide shipping expenses and responses from procurement manager surveys, signalizes that the stresses on the supply chain that sprouted amid the COVID-19 crisis and boosted global inflation are noticeably relaxing. The untangling of these supply chain knot spots is projected to relieve inflationary pressures on a worldwide platform. Nonetheless, remaining alert and overseeing forthcoming advancements is critical to ensure the endurance of these supply chain enhancements and their prolonged bearing on inflation.

The insights gleaned from the Global Supply Chain Pressure Index radiate a hopeful beacon that the tribulations plaguing supply chains, inclusive of disruptions and limitations, are being effectively tackled. By navigating these chokepoints, we look to a global economy graced by enhanced proficiency and firmness. However, ceaseless surveillance and forward-thinking maneuvers will be essential to warrant that supply chains uphold resiliency and remain agile to future upheavals.

World trade volume growth to slowdown in 2023

International commerce faces strains from geopolitical unrest, diminishing worldwide demand, and stricter monetary and fiscal plans. The volume of global trade encompassing both goods and services is predicted to witness a merely 1.7% expansion in 2023, a dip from the 2.7% growth registered in 2022. Concurrently, the World Trade Organization (WTO) has revised upward the anticipated growth in global trade volume to 1.7% in April 2023, from the initial 1% projected in October 2022, spurred by elevated estimates for global economic growth.

Forecasts for 2023 place North America in the lead for merchandise export expansion (3.3%), trailed by Asia (2.5%), and Europe (1.8%). Sluggish export growth is envisioned in the Middle East (0.9%) and South America (0.3%), while Africa is likely to see a contraction in goods exports (-1.4%).

The International Maritime Organization (IMO) has charted course for achieving net-zero carbon emissions by 2050 in the shipping sector, while the European Union aims to enforce a carbon levy on inbound and outbound shipping starting 2027. These steps are predicted to escalate the expenses for globally traded import and export products by 3% to 4%, equivalent to an annual cost of $600 to $800 billion.

Mexico has outmatched China as America's principal trade ally, marking $263 billion in goods trade between the two nations in the initial four months of 2023, as per the Federal Reserve Bank of Dallas. This shift underlines the sustained impact of the economic disruptions from 2020 on the global economy and pinpoints the brisk turnover in international trade dynamics.

Unemployment rate by region and age demographic

Per the International Labour Organization (ILO), the aggregate jobless rate for people aged 15 years and over is anticipated to climb in the Americas (from 5.8% in 2022 to 6.1% in 2023), the Arab States (from 9.3% to 9.4%), and Europe and Central Asia (from 6.1% to 6.3%) due to the forecasted economic deceleration. The ongoing economic downswing intimates that many workers might be compelled to settle for jobs of inferior quality marked by low remuneration and inadequate hours. The escalating cost of living, contrasted with nominal work income, presents a potential hazard of thrusting more individuals into impoverishment. However, in the Asia-Pacific region, the unemployment rate is predicted to recede to 5.1% in 2023, down from 5.2% in 2022, propelled by an economic resurgence.

Youth unemployment continues to pose a significant worldwide concern. Youngsters, particularly those aged 15-24, grapple with substantial hurdles in securing and retaining respectable employment. Their rate of unemployment is nearly triple that of adults. In 2023, the Arab States are projected to exhibit the utmost rate of youth unemployment at 26.7%, succeeded by the Asia-Pacific region (15%), Europe and Central Asia (14.8%), the Americas (13.8%), and Africa (11.2%).

Key Macro-indicators outlook

Global economic outlook

According to the International Labour Organization (ILO), unemployment for those 15 years and older is set to rise in the Americas, Arab States, and Europe and Central Asia due to expected economic slowdown. Contrarily, Asia-Pacific's rate is predicted to decline, owing to economic revival. Young people aged 15-24 globally face significantly higher unemployment rates, with the highest predicted for the Arab States in 2023.

Quarterly GDP Trends

Projections show all G7 countries, except Germany, Canada, and Sweden, reported positive economic growth in Q2 2023. These three countries are expected to face challenges due to raised policy interest rates and reduced demand. The US GDP growth is projected to stagnate and diminish slightly in Q3 and Q4 2023, respectively, due to factors like high inflation, banking crisis, and decreased government spending. Conversely, Japan's economy shows moderate recovery, while China's strong rebound is anticipated to slow down due to sluggish demand, investment cuts, and high youth unemployment. India's economy is likely to see a slight slowdown in H2 2023 due to reduced external demand, despite solid domestic demand.

Inflationary pressure to ease but to stay above central banks target in 2023

US consumer price inflation decreased to 4.0% in May 2023, with predictions suggesting it will ease further from 8% in 2022. In the Eurozone, inflation is expected to relax to 5.2% in 2023 from 9.4%, despite France, Germany, and Italy projecting figures above the Eurozone's 2% target. The UK's inflation rate is anticipated to drop to 7% in 2023 from 9.1%, remaining significantly above the Bank of England's target. Meanwhile, India has witnessed a decline in annual inflation, which falls closer to the Reserve Bank of India's target, forecasting an ease to 5.1% in 2023 from 6.7% in 2022.

Industrial production trend in major economies

Businesses in 2023 face various struggles amid a volatile global economy, increasing costs, and geopolitical unrest. Solutions involve diversifying suppliers and adopting innovative business models like e-commerce to cater to evolving consumer taste. A shortage of skilled workers further hampers growth, necessitating comprehensive training programs.

In industrial production trends, US manufacturers grapple with weaker domestic demand and concerns of global economic slowdown. Industrial growth was sluggish in Q1 2023 at 0.8%.

On the other hand, German industry experienced a rebound with 2% growth in Q1 2023, driven by backlogged orders and easing supply issues.

In contrast, the UK's industrial output declined in April 2023, marked by decreases in manufacturing, mining and quarrying, and water supply and sewerage.

In Q1 2023, France's industrial output fell due to social unrest, but saw a resurgence in April across all sectors. However, Italy and Belgium experienced contractions in the same period, with a significant decline in Italy in April. In contrast, the Dutch manufacturing industry saw a substantial drop, marking the largest decrease since 2009.

Switzerland's industrial growth was buoyed by strong international demand early in 2023. Sweden also demonstrated industrial growth in Q1 2023, but economic challenges led to a contraction in March.

Chinese industry continued its growth, albeit at a slower pace, while Japan saw slight growth in April, breaking a series of contractions. India demonstrated accelerated industrial growth, driven by a surge in factory activity in April 2023.

Public Finance

Global debt exhibits rising trend

Global debt reaches a near-record high of $305 trillion in Q1 2023. High-interest rates strain developing countries and lead to higher debt servicing costs, according to IIF.

In 2023, developing nations are under pressure due to rising interest rates and lowered exchange rates, leading to an increase in global debt as these countries borrow at higher costs. Global debt nearly peaked at $305 trillion in Q1 2023, with worries about increasing debt servicing costs and possible risks in the financial system.

The IIF, highlighting the potential for a credit crunch, noted an escalated overall debt in emerging markets, reaching a record $100 trillion in Q1 2023. Contributors include not just developing countries but also developed ones like Japan, the US, France, and the UK.

Governments are strained with growing expenses from factors such as aging populations and healthcare costs. Increased defense expenditures due to geopolitical tensions could impact credit profiles. The US resolved its debt ceiling crisis in June 2023 and temporarily suspended it until 2025 to avoid severe economic consequences.

Stock market trends

Major stock indices show an improving trend

The US stock market demonstrated remarkably strong performance in H1 2023, irrespective of recession fears, buoyed by declining inflation. European stocks also rallied, bolstered by China's positive economic outlook despite concerns about Eurozone inflation.

Despite modest gains, the potential for Asian markets to exceed global performance remains, given their superior fiscal sustainability, inflation control, and financial system health due to limited quantitative easing.

India's equity market is thriving, becoming the fourth largest globally behind the US, China, and Japan. Despite global economic uncertainties, India's benchmark indexes have skyrocketed, exceeding European markets and pushing the total value of Indian equities to $3.5 trillion. This success is credited to India's strong economy, expanding middle class, growing manufacturing sector, and large population.

The financial landscape in the first half of 2023 has been dynamic, marked by a surge in AI technology, upheaval in commodity markets, a revival in cryptocurrencies, and a notable banking downturn. This AI wave, spearheaded by entities like Meta, Tesla, and Nvidia, contributed significantly to the growth of major tech companies. Yet, fears of a possible bubble persist as these companies would need substantial profit growth to validate their elevated valuations.

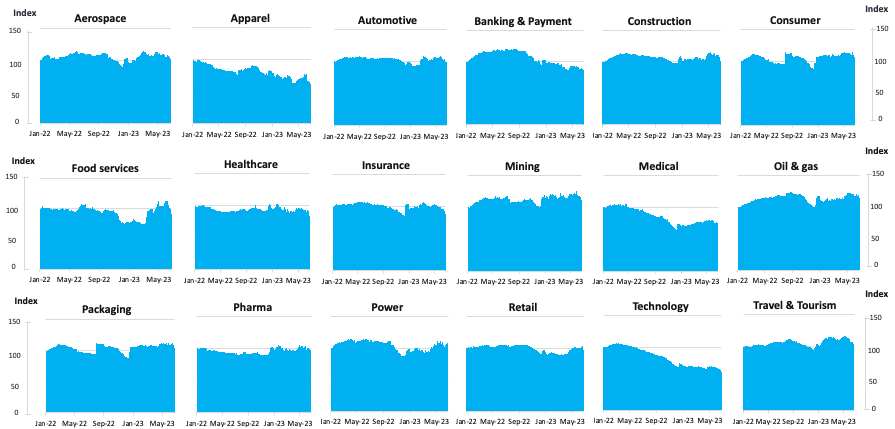

Equity, M&A deals & active jobs by sector

Recent months have seen fluctuating trends in equity indices.

M&A deals index

Active jobs exhibit varying trends sector-wise

World Economic Outlook

2023 kicked off positively for the global economy, spurred by factors like reduced energy prices and China's reopening. However, regional differences are expected due to varying business cycle stages, with APAC forecasted to perform well and Western nations experiencing projected slowdowns.

Lower energy costs and improved supply chains have led to decreased headline inflation rates in developed nations, but persistent robust wage growth keeps core inflation high, prompting cautious central bank policies.

In response to inflation, central banks, including the US Federal Reserve and European Central Bank, have tightened monetary policies by raising interest rates. However, some may pause for impact assessment before further adjustments.

Positive trends are observed in certain financial market sectors, with equities showing strength, especially in Europe, and bonds rallying due to expectations of inflation decline and interest rate hike pauses, creating investment opportunities in emerging market equities and growth-oriented fixed income segments.

Nevertheless, risks include potential contagion from issues in US regional banks leading to a broader credit crunch and steady core inflation rates creating a need for extended high-interest periods or further rate hikes. Geopolitical tensions, such as those between the US and China and ongoing conflicts in Ukraine, also pose risks through potential trade restrictions, military confrontations, and associated uncertainties impacting political and economic stability.

Final Thoughts

In conclusion, the uptick in the global economic growth projection for 2023 is a hopeful sign of recovery and resilience. This positivity is largely fuelled by the impressive economic performance of various regions, particularly the Asia-Pacific nations like India and China. However, it's vital to note that not all regions share in this upward trend, with areas like the Middle East and Africa still grappling with challenges. The volatile variables of energy and food prices serve as crucial reminders of the interconnectedness of our global economy. Therefore, while we rejoice in the positive forecast adjustments, we must remain dedicated to mitigating inequalities and prioritizing sustainable development. After all, our global economy is only as robust as our most vulnerable regions, and each step forward should drive us to support those still striving to catch up.